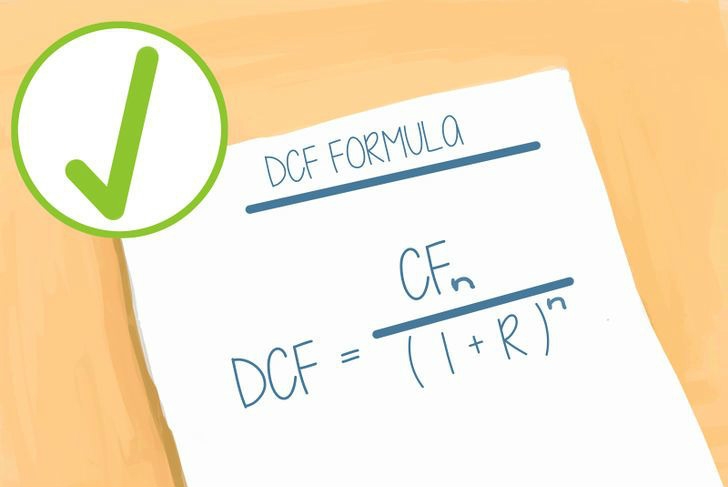

For those that don’t live and breathe financial jargon, a DCF (discounted cash flow analysis) is a method of calculating the present value of a future benefit and they are often used whenever someone needs to figure out a justifiable valuation for something that doesn’t have a ready market value (and sometimes looking for valuation mistakes in things that do). There are several other common valuation methods as well, including: Comparable Sales, Replacement Cost, Book Value, but for certain applications a DCF is very helpful.

The most common reason I will use a DCF is for determining pre/post money valuations for startups, since they by definition have little more than pro-forma financials.

In preparing a DCF for a startup I need to know the expected cash flows and the appropriate discount rate. I can pull the expected cash flows from the pro-forma financial statements, but the discount rate is really mine to decide. As a definition, the discount rate is: “the rate of return that could be earned on an investment in the financial markets with similar risk.” (Wikipedia)

With that rate in mind, I have typically used 27% as my discount rate for startup companies. Why 27%…because the Marion Kauffman Foundation published a report in November of 2007 based on their research that indicated a national average IRR (internal rate of return) of approximately 27% on angel investments. I haven’t seen anything since then that would purport to be a better number, so that is still what I use.

Of course a lot has changed in the economy since November 2007, so I wonder what others are using for a discount rate now or if that metric still holds true?